Cellnex Telecom SA

110 Billion (30 Year) backlog trading at 9% normalised FCF yield

Business Overview

Cellnex is Europe’s largest telecommunications towers and infrastructures operator, enabling operators to access a wide network of telecommunications infrastructures on a shared-use basis, and thus helping to reduce access barriers and to improve services in the most remote areas.

The Company manages a portfolio of more than 130,000 sites, including forecast roll-outs up to 2030, in 10 European countries, with a significant footprint in Spain, France, the United Kingdom, Italy and Poland. Cellnex holds a dominant market share in the countries that they operate in and is the market leader in 7/10 countries that they operate in and ranks the top 3 in market share for all 10 countries.

The company operates multiple business segments including the following:

Towers (81% of Revenue): Passive infrastructure services for MNOs(mobile network operators) and other wireless operators.

DAS, Small Cells & RAN-as-a-Service (7% of Revenue): Solutions for high-density urban areas and indoor coverage (stadiums, tunnels), including active equipment management in Poland.

Fiber, Connectivity & Housing (6% of Revenue): Data transport (FTTT), backhaul, and edge data center hosting to support 5G capacity.

Broadcast (7% of Revenue): Digital TV and radio broadcasting services, primarily in Spain.

Understanding Tower Operators and why the business exists?

Tower operators are responsible for building as well as maintaining telecom towers that are used everyday by millions of users. The main customers of tower operators are the telco companies.

In the markets that cellnex operators, their main customers are as follows:

France: Bouygues, Iliad, Orange, and SFR.

Italy: Iliad, Fastweb, Vodafone, Linkem, TIM, and WindTre.

United Kingdom: Virgin Media O2 (VMO2) and Vodafone.

Spain: Telefónica

Poland: Polsat

Netherlands: Odido

Portugal: Digi

Due to the nature of the industry (slow growth rate, high initial capital required to enter the industry), the competition of the telco industry is limited and what is occurring currently in the EU is the consolidation of the telco companies into a single company.

To explain why cellnex’s business model exists, we have to first understand more about how the telco companies used to operate in the past.

Telco in the 2000s was a booming industry as we were at the beginning of an internet revolution. Mobile penetration was low and the world was largely analog. With the advent of the internet and the PC, the telco industry became a fast growing industry that attracted many competitors that laid out cables and towers in order to “meet” the forecasted demand. As we all know, that demand did not materialise. The high capital expenditure nature of their business models lead to numerous telco companies going bust when revenues did not materialize. Over the last 10 years, a new trend has emerged. Instead of the usual capital expenditure heavy business models, telco companies seek to revamp their business models into capital asset light models and offloaded the building of the towers and cable to towercos such as cellnex. Building and maintaining physical towers is extremely capital-intensive (CapEx). Telcos are increasingly under pressure to invest billions in spectrum licenses and active network equipment (5G hardware). By selling their tower portfolios to a TowerCo, Telcos receive a massive cash infusion that can be used to pay down debt or fund 5G rollouts. Infrastructure generally yields a lower, stable return. By moving these assets off their balance sheets, Telcos can improve their financial ratios and focus their capital on high-margin services like data plans, fiber, and customer experience. In exchange for offloading the towers to towercos, telco companies will sign long term contracts (20-30 years) with the towerco companies. This enables them to treat the towers as an operating expense instead of capex and at the same time reduces the need for the telco companies to take on large amounts of debt.

Why are towercos such good businesses?

The main reason why the towerco industry caught my attention was because of the extremely high barriers to entry to the industry. In an industry where physical presence is everything, the barriers to entry are not just financial, but are deeply rooted in regulatory, geographic, and social constraints. These factors ensure that once a TowerCo establishes its footprint, it becomes nearly impossible for a new competitor to disrupt its dominance.

Infrastructure Monopoly

The primary barrier to entry is the extreme difficulty of obtaining permission to build towers. Unlike digital businesses that can scale easily, a TowerCo is tethered to the physical world of Zoning and Regulation. Local governments and municipalities treat tower permits with intense scrutiny, often requiring months or years of bureaucratic navigation.

This barrier is further reinforced by “Not In My Backyard” (NIMBY) sentiment. Residents generally desire high-speed connectivity but are often vocal opponents of new industrial structures in their neighborhoods. These social and legal hurdles act as a natural cap on supply. For an incumbent like Cellnex, every existing tower is a pre-approved asset that cannot easily be replicated, making the existing portfolio increasingly valuable as the demand for connectivity grows and the supply of new permits tightens.

Beyond regulation, the TowerCo business is governed by the laws of physics and geography. A tower’s value is derived entirely from its strategic location. To provide effective coverage, a tower must occupy the high ground which can be a literal hilltop (Bukit Timah hill & Sentosa for Singapore) or a prime urban rooftop.

In most high-demand areas, there is a finite amount of space that offers the necessary line-of-sight for radio signals. Once a TowerCo secures the optimal site within a specific radius, there is often no economical reason or legal room for a second competitor to build a rival structure nearby. This creates a “natural monopoly” at the micro-level. A competitor cannot simply build a tower 50 meters away; even if they could find the land, the regulatory authorities would likely deny the permit on the grounds of visual pollution and redundancy, forcing the newcomer to instead rent space from the incumbent. Once the minimum efficient scale for a particular country is reached, the company will achieve a natural monopoly.

Inflation adjusted revenues with clear backlog visibility

The other trait of the towercos that attracted me to the industry is the unique contractual framework that governs its revenue. By providing mission-critical infrastructure, companies like Cellnex command pricing power and a degree of stability rarely seen in other sectors. This stability is built on three pillars: high customer stickiness, multi-decade contract durations, and built-in protections against macroeconomic volatility.

In the telecommunications world, a tower is not merely a piece of real estate but it is a vital node in a live network. For a mobile operator, the prospect of moving equipment from one towerco to another is a logistical and financial nightmare as they would have to 1) employ a tower co to build new towers which requires high upfront costs and/or 2) Pay a breakup fee equal to the remainder of the revenue of the contract. Such a move is highly illogical especially considering the risk of localized service outages, and the potential for coverage holes that frustrate subscribers.

Consequently, the churn rate, the percentage of customers who leave, is incredibly low, typically staying from 1% to 2% (cellnex has a churn rate of 1.2%). Once an operator installs its antennas on a tower, it effectively becomes a tenant for life and is likely to renew its contracts 30-40 years down the road. This stickiness transforms the TowerCo’s revenue from a series of individual transactions into a highly reliable, recurring annuity.

Unlike typical commercial real estate where leases might be renewed every three to five years, Cellnex operates on Master Service Agreements (MSAs) that are 20-30 years long.

This long-term horizon provides the business with unparalleled revenue visibility. The business model of cellnex enables the company to essentially secure a guaranteed cash flow stream that will last through multiple economic cycles. In my opinion, this makes the business model behave more like a high-yield infrastructure bond than a traditional stock. The predictability of these 20-year contracts allows TowerCos to plan long-term capital deployments and dividend policies with extreme confidence. The certainty of the revenue streams also enable the towercos to take up large amounts of debt to fund their capital expenditures to build towers. In the case of Cellnex, the company has a revenue visibility via their backlog of over 30 years (110 Billion ex escalators on a 4B ARR). This backlog is the longest and the largest in the industry.

Lastly, Cellnex’s business model also offers a rare natural hedge against rising costs. The MSAs for cellnex include escalator clauses, which are contractual mechanisms that automatically increase the rent every year. These increases are typically tied to the Consumer Price Index (CPI) or a fixed annual percentage (e.g. 2%). Cellnex’s revenue contracts are split where 65% of the contracts are CPI linked and the other 35% are annual escalators of 1-2%. Cellnex’s contracts are capped on the downside (i.e. if there is deflation, the rent of the towers will not decline). These inflation-indexed contracts ensure that the business’s real margins are protected, regardless of the macroeconomic environment. While traditional businesses may struggle to pass on costs to consumers during inflationary periods, the TowerCo’s price increases are baked into the contract by design. What makes the business model of cellnex even more attractive is the fact that the company passes through electricity and utility costs, making the company immune to oil shocks and energy volatility. The only costs that the company is responsible for are land lease, labour and maintenance costs for the towers.

Understanding the shifts in the telco industry and why cellnex will benefit significantly from it.

Transition from 4G to 5G

Unlike America, Europe has yet to adopt 5G to a large extent. By early 2026, all three major US carriers (T-Mobile, Verizon, and AT&T) have officially launched nationwide 5G SA cores, enabling the united states to have 90% of the networks to have 5G capabilities as compared to Europe’s 40%. The strategic importance of 5G capabilities lies in their role as the connective tissue for the next generation of global economic productivity. Beyond simply increasing mobile download speeds, 5G Standalone architecture introduces ultra-low latency and massive machine-type communications, which are essential for the integration of Artificial Intelligence into the physical world as well as the utilization of AVs. The transition to 5G is expected to cause the average consumption to grow from roughly 15 GB/month in 2022 to 80-90 GB/month by 2030, marking a 28% CAGR.

So how will this benefit cellnex?

The most immediate benefit of 5G for Cellnex is the mandatory requirement for network densification. Because 5G operates on higher frequency bands that have a shorter propagation range and struggle to penetrate physical obstacles, mobile operators can no longer rely on a sparse network of large macro towers. To provide consistent coverage, they must deploy thousands of additional “points of presence” (PoPs). This forces operators into two paths, both of which favor cellnex:

They must either rent additional space on existing Cellnex towers (Colocation)

Commission Towercos like Cellnex to build new sites through Build-to-Suit (BTS) programs.

In 2025 alone, Cellnex saw its organic PoP growth rise by 4.5%, a direct result of tenants adding 5G equipment to existing sites. The 4.5% growth in revenue might seem minimal but in reality, it creates significant profit growth for the company especially if the clients choses option (1)-colocation.

Before I move on to explain what colocation means, I would also like to point out the second trend that is emerging.

(2) Increasing willingness for telco companies to share network infrastructure aka colocate

In the early days of mobile (2G and 3G), the product was the signal itself. If a Telco had a tower in a rural area where its competitor didn’t, it could charge a premium and steal customers. Coverage was a unique selling point. However, network coverage has now reached parity in Europe. Every major carrier has a signal in almost every city. Since you can no longer win customers just by having a tower, there is no longer a competitive advantage in owning the physical steel in the ground. Telcos now compete on brand, content, AI services, and customer experience instead.

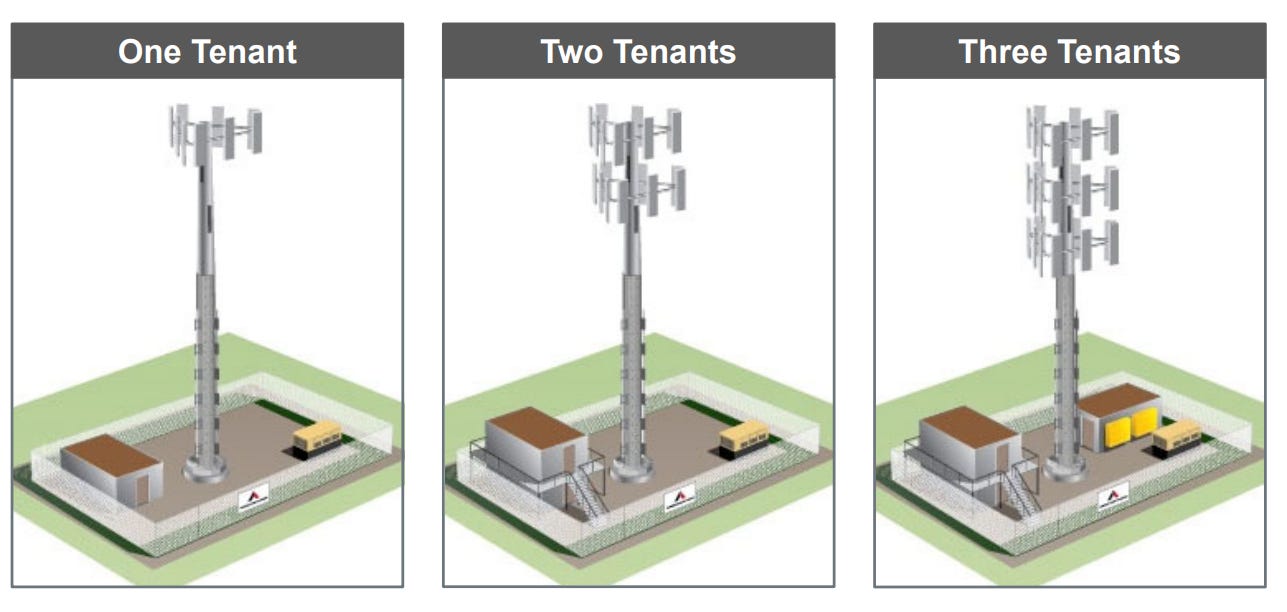

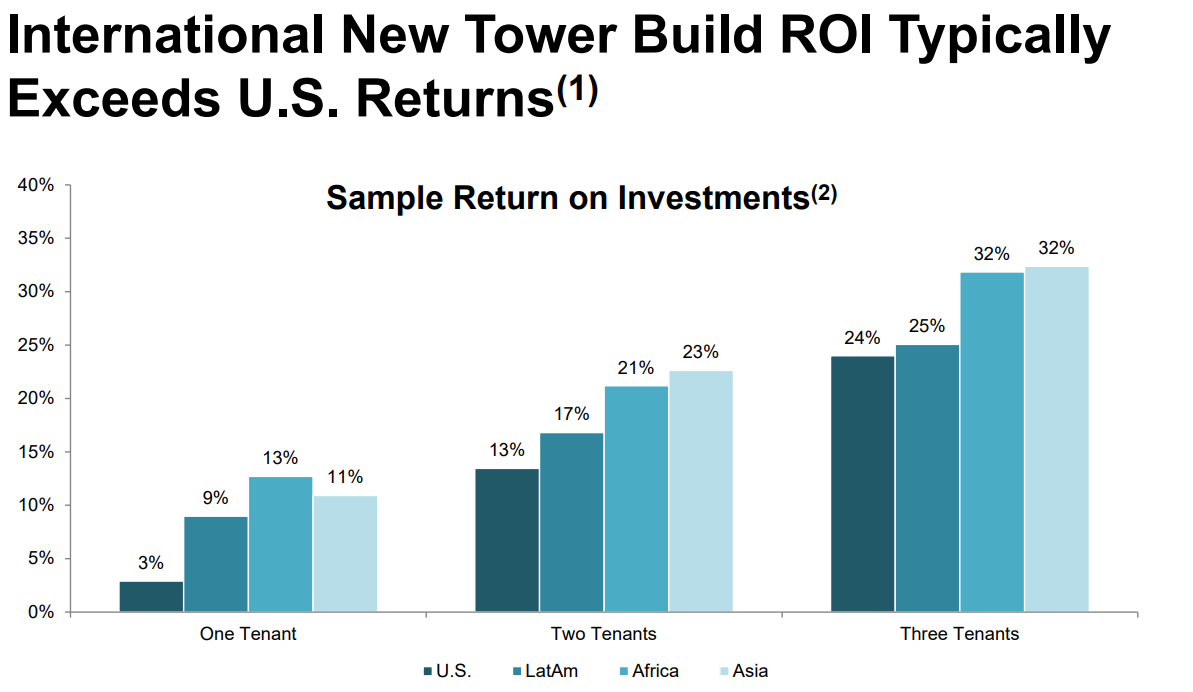

To understand why colocation is hugely beneficial for the business below is an image to make it easier to visualise:

Collocation is a situation where there are more than 1 client sharing the cell network. To build a tower, the main cost associated with it is the building of the stem (the core structure). In order to house more tenants, the tower companies only have to add an additional antenna on the cell towers to bring in more revenue. To add the second client onto the tower, the cost is minimal considering that the land leases and the infrastructure costs and maintenance costs of the towers need to be paid for regardless of whether there are 1,2 or 3 clients. This means that almost all of the additional revenue gained from the new client (about 95%) flows directly to the bottom line of the company.

Cellnex currently has a tenancy ratio of 1.6 (which means that there are approximately 1.6 tenants per tower that they own across the 113K towers). We can estimate that the ROI of the capex that they deploy for the towers is likely to be around 15%.

Colocation will be one of the key drivers of the growth for the company in the long term.

The Origins Of Cellnex

The foundations of Cellnex were laid within Abertis Infraestructuras, a Spanish conglomerate primarily focused on toll roads and parking management. For years, the telecommunications arm operated as “Abertis Telecom,” managing broadcast towers and terrestrial television signals in Spain. However, by 2014, the strategic decision was made to spin off this division to capitalize on the burgeoning demand for mobile data. In May 2015, the company rebranded as Cellnex Telecom and launched its Initial Public Offering (IPO) on the Spanish stock exchange at a valuation of approximately €3.2 billion. This independence was the crucial catalyst; as a neutral player no longer owned by a specific phone company, Cellnex could market its tower space to all competing mobile operators without conflict of interest.

Era of Hyper-Expansion (2015–2022)

Following its IPO, Cellnex embarked on one of the most aggressive acquisition sprees in European corporate history. Led by CEO Tobias Martinez, the company recognized that the European tower market was highly fragmented compared to the United States. Cellnex utilized a Build-to-Suit and acquisition model, buying thousands of towers from operators like Wind Tre in Italy, Bouygues Telecom in France, and Sunrise in Switzerland.

The defining moment of this era occurred in 2020, when Cellnex reached a landmark €10 billion deal with CK Hutchison to acquire approximately 24,600 towers across six European countries, including the UK, Ireland, and Austria. This move solidified Cellnex’s position as a pan-European titan. By the end of 2022, the company had grown its portfolio from roughly 7,000 towers at its birth to over 130,000 sites across 12 countries, supported by a series of massive rights issues that demonstrated deep investor confidence in the TowerCo model. This aggressive acquisition period was emboldened by cheap capital with interest rates close to 0. This aggressive expansion plan caused the company to be laden with debt and the company also diluted its shareholders significantly.

Pivot From Growth to Investment Grade

By late 2022 and early 2023, the global macroeconomic environment shifted. Rising interest rates made the debt-fueled acquisition model more expensive. In response, Cellnex announced a fundamental shift in its strategy and chose to move from inorganic growth (buying more towers) to organic value creation and debt reduction. The company committed to achieving an Investment Grade credit rating from S&P, focusing on increasing the tenancy ratio of its existing towers rather than adding new ones (via BTS) that are beneficial to revenue but do not increase profitability by much. This period also saw a leadership transition, with Marco Patuano taking over as CEO to oversee this more disciplined financial phase.

The Pivot to Shareholder Yield

Having achieved its goal of becoming Europe’s largest independent tower operator, Cellnex has pivoted its entire corporate strategy toward maximizing shareholder yield and capital returns. Having successfully consolidated a pan-European portfolio of over 130,000 sites, Cellnex has moved into what management defines as Chapter 2 of its corporate history. As of 2026, the company has pivoted and is focusing instead toward the maximization of shareholder yield and the aggressive generation of Free Cash Flow (FCF).

In fiscal year 2025, Cellnex demonstrated its commitment to returning capital ahead of its original 2026 schedule, delivering a combined total shareholder yield of approximately 6.5%. This was achieved through a dual-track strategy of dividends and buybacks. The centerpiece was an €800 million share buyback program that saw the company repurchase approximately 24 million shares. By reducing the total share count, Cellnex achieved a 16.7% growth in Recurring Levered Free Cash Flow (RLFCF) per share.

This transition to a yield-focused model is further supported by a rigorous commitment to an Investment Grade (BBB-) credit rating. By the first quarter of 2026, Cellnex successfully brought its Net Debt to EBITDA ratio down toward a 6x target, a significant reduction from the high-leverage era of 2021. This de-leveraging was accelerated by the strategic divestments of non-core assets, including the 2025 sale of French data centers and other peripheral infrastructure. The company also initiated a €500 million dividend distribution from the share premium reserve, split between January and July 2026.This transition represents a shift in the stock’s DNA: from a volatile, high-beta growth play into a defensive, bond-proxy asset that offers both the stability of 30-year contracts and a growing yield profile.

Looking forward through 2026 and beyond, Cellnex has established a permanent “floor” for shareholder remuneration. The company has committed to a minimum of €1 billion in annual returns, split evenly between dividends and opportunistic buybacks. This dividend is projected to grow at a minimum of 7.5% annually through 2030, a rate secured by the inflation-linked escalator clauses and 5G densification mandates built into its Master Service Agreements.

Investment Thesis

Rapid FCF Expansion As BTS Scales Down

Cellnex reports its annual report using special terminology to better reflect the company’s financial situation. Seeing the company using the GAAP metrics will not give a proper understanding of the company and how it operates. I will be defining each of the terms that cellnex uses and give you a brief explanation of why the metrics are used instead.

1. Revenues (ex Pass-through)

This is the “clean” top-line number. Cellnex often pays for the electricity and ground rent at their sites and then bills that exact amount back to the telcos. The cost of electricity and energy will be passed through to the customers.

To calculate revenue (ex pass through) it is = Total Operating Income minus Pass-throughs (utilities, energy, and business rates) and Advances to Customers.

Since pass-throughs have zero margin and can be volatile (like energy prices), Cellnex strips them out to show the actual “rental income” they are earning from their tenants.

2. Adjusted EBITDA

This is their primary measure of Operating Profit before the heavy costs of their massive debt and tower leases.

Operating Profit before Depreciation and Amortization (D&A), adding back non-recurring items (like redundancy provisions or M&A costs) and non-cash expenses (like share-based compensation).

Adjusted EBITDA shows the cash-generating power of the towers themselves, independent of how they were financed.

3. EVITDAAL(EBITDA after Leases)

This is arguably the most important operational metric for a TowerCo.

Adjusted EBITDA minus Lease Payments (the rent Cellnex pays to the landlords who own the land under the towers).

Unlike a typical company where a lease is just an expense, Cellnex’s business is all about the spread between what they collect from telcos and what they pay to landowners. EBITDAaL shows the profit left over after paying their own landlords.

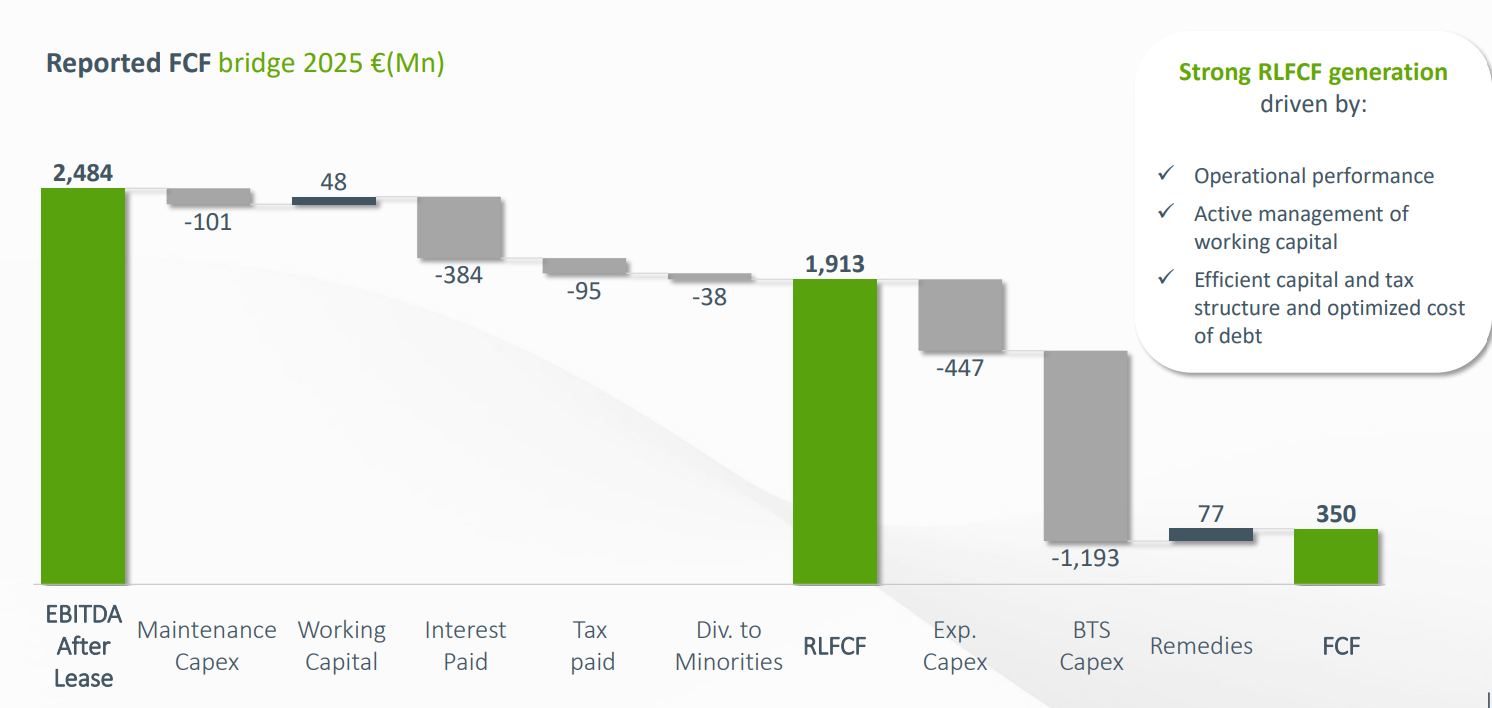

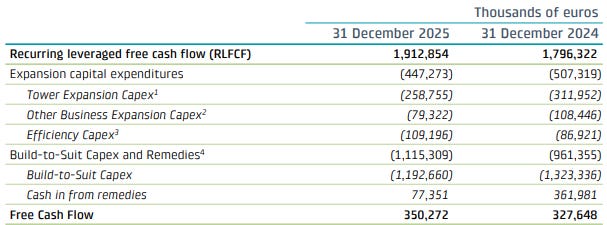

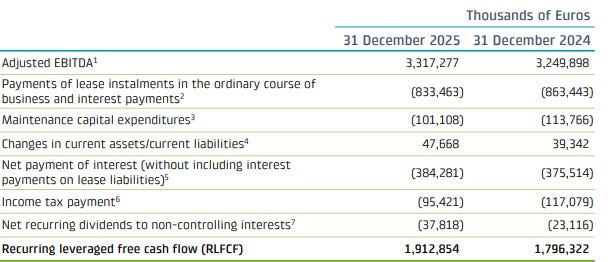

4. RLFCF (Recurring Levered Free Cash Flow)

RLFCF represents the cash available for shareholders in a normal year.

To calculate RLFCF it is = EBITDAaL minus Net Interest Paid (the cost of their debt) minus Maintenance CAPEX (money spent just to keep the towers from falling down) minus Income Tax Paid plus/minus Changes in Working Capital

It ignores Growth CAPEX (buying new towers) and focuses only on the cash generated by the existing portfolio.

5. FCF (Free Cash Flow)

This is the Bottom Line of the cash flow statement.

RLFCF minus Growth CAPEX (Expansion CAPEX and Build-to-Suit programs).

In the Hyper-Growth phase (2015–2022), this was often negative because Cellnex was spending billions to buy towers. In the 2025–2026 Value Phase Cellnex has pushed this to be slightly positive, as they are spending less on acquisitions and more on returning cash to shareholders.

Understanding the BTS model

Recall earlier that I stated that in order to meet the customer’s demand, cellnex has 2 choices: BTS and colocation. In the Cellnex model, BTS represents a contractual commitment where a mobile operator (like Vodafone or Orange) asks Cellnex to build a brand-new tower in a specific location where they currently have a dead zone or need 5G densification. Instead of building it themselves (which would sit on their own balance sheet and require high CAPEX), they ask Cellnex to do it. Cellnex will then find the land, get the permits, and build the steel structure after the mobile operator signs a 20-30 year lease with cellnex. As I mentioned earlier, colocation is a much more profitable venture for cellnex as the ROI from such an investment is higher. However the current BTS obligations are actually obligations that have been collected during the heavy acquisition era of cellnex. As of early 2026, Cellnex has a massive BTS backlog of approximately 15,000 to 20,000 committed sites to be built through 2030. Cellnex BTS backlog is expected to taper off to 0 from the current 1.2B euros after 2030 with the bulk of which being completed in 2028 which will be highly accretive to FCF.

FY 2025 annual report

The current FCF of the company is understated due to the fact that Cellnex has to still fulfil these BTS obligations. BTS obligations will have a diluting effect on cellnex’s tenancy ratios as the new BTS sites will only have a tenant ratio of 1. However, over the next 3 years, cellnex will be able to onboard other mobile operators onto the BTS towers that they have built and increase the tenancy ratios back towards their targeted goal. If we actually normalise the FCF of the company, the company is now generating approximately 1.55B in FCF on a market cap of 18B representing a FCF yield of 8.6%. Considering the aforementioned traits of the company, the company is trading at an absurdly cheap valuation especially considering the fact that other similar TowerCos such as AMT and INWIT are trading at 4.5% and 6.5% fcf yield respectively and Cellnex’s own towers were sold at a 4% ULFCF yield to private equity.

I’d like to take a moment to talk about INWIT which is a company that is very well run and has margins that I expect Cellnex to be able to achieve over the next few decades. INWIT consistently maintains one of the highest tenancy ratios in the world. As of Q3 2025, their ratio stands at 2.37x and the company’s long-term business plan aims to reach a tenancy ratio of 2.60x by 2030. Unlike Cellnex, which often buys single-tenant towers and then works to fill them, INWIT was born from the merger of the tower portfolios of TIM and Vodafone Italy. This gave them an immediate anchor of two massive tenants on nearly every tower from day one. Unfortunately, this causes the company to have high exposure to 2 companies that contribute 90% of its revenues. Furthermore due to its customer base, the growth path of the company is limited considering that competing companies’ mobile operators will not be willing to utilities their towers as they are run by the competitors. Cellnex on the other hand is a neutral operator and provides its service to every single major operator. Furthermore, Cellnex also has a larger TAM considering that it serves the pan European market whereas INWIT only serves the Italian market. Another key issue that Inwit faces is the concentration of the revenue from the 2 customers TIM and Vodafone who represent 90% of their revenues. Should the customers decide to not renew the contracts, INWIT will be hit severely (Update: Vodafone and Tim are threatening to break the MSA contracts). Cellnex on the other hand has numerous customers across 10 countries, thus the concentration risk for the company in terms of geography and customers are lower.

Valuation mismatch between Private and Public Markets

Cellnex over the past 2 years have divested the cell towers that they owned in countries where they are not the market leader. A tower, once constructed, demands a largely invariant cost base. A site technician must periodically inspect and maintain it regardless of whether one or three operators have equipment installed. A field engineer must respond to faults and perform equipment swap-outs whether the site generates €20,000 or €60,000 in annual revenue. A lease manager must administer the ground lease with the underlying landlord irrespective of tenancy. Regional operations managers, network operations centres, and the full apparatus of central functions such as finance, legal, regulatory, HR all exist as overhead that the portfolio must absorb. None of these costs scale meaningfully with incremental tenants.

This logic, however, only functions efficiently when the portfolio is dense enough within a given geography. A regional operations manager overseeing 1,500 sites in a compact market commands a meaningfully lower cost per tower than one overseeing 150 sites in the same country. Ground lease negotiations carry far greater counterparty leverage when the operator controls hundreds of sites and represents a meaningful share of a landlord’s portfolio than when it controls a token presence. The minimum viable cost of operating in a country is largely fixed regardless of portfolio size. This is the country’s overhead problem, and it is the mechanism through which thin market presence destroys unit economics. A 200-tower footprint in a given country bears a country cost structure that is not radically lower than a 2,000-tower one, yet it generates a fraction of the revenue.

It is precisely this logic that underpinned Cellnex’s strategic pivot and its associated divestitures. Having spent 2015-2022 acquiring towers across Europe in an era of cheap debt and accumulating positions in over a dozen markets. Cellnex found itself, by the early 2020s, holding a portfolio that was deep and competitive in some geographies and thin and subscale in others.

Markets such as Ireland and Austria, where Cellnex’s footprint was relatively modest compared to incumbent players, were identified as candidates for disposal. The capital repatriated from these exits were redeployed to reduce leverage, share buybacks as well as reinvested in markets such as Spain, Italy and France where Cellnex commands scale economics, dense portfolios, and the operational leverage to convert incremental tenancy into near-pure margin.

How Much Are Private Equity/Competitors Paying For Cellnex Towers?

1. France — Phoenix Tower International (PTI) + Bouygues Telecom JV

Towers: 3,226 sites

Valuation: €620 million priced at 24X EBITDaaL

Due to the aforementioned benefits of scale, competitors in the country are willing to pay high prices for extra towers in the geography where they have scale.

2. Sweden & Denmark (Cellnex Nordics) — Stonepeak (49% stake)

Towers: 4,557 operational sites + ~2,500 pipeline sites

Proceeds: €730 million (for the 49% stake, implying ~€1.49 billion enterprise value for 100%) EV/EBITDAaL: 24x 2024E EBITDAaL (acquisition was done in 2023)

3. Ireland — Phoenix Tower International (100%)

Towers: ~1,900 sites (~1,700 towers + ~200 land locations)

Proceeds: €971 million EV/EBITDAaL: ~24x EBITDAaL

Towers: ~4,600 sites

Proceeds: €803 million (including €272 million deferred to December 2028)

EV/EBITDAaL: Just over 20x, based on 2023 EBITDA

5. Switzerland — Process Ongoing

Towers: ~6,000 radio sites (Cellnex holds 72%; Swiss Life Asset Managers holds 28%)

Expected Proceeds: Up to ~€2 billion for Cellnex’s 72% stake

Implied EV/EBITDAaL: Cellnex refusing to sell stake unless “private markets overpay” (based on Marcos’s statements) Expected EV/EBTDAaL is 26.

As we can see from the past divestitures to companies and private equity, they are valuing the company’s towers at the Mid 20s EV/EBITDAaL multiples. However, the market is currently valuing cellnex as a whole at just 13.5 EV/EBITDAaL. This clearly shows that there is a disparity between the public markets from the private markets that signals potential undervaluation and potential value unlock as the company continues to divest its towers where it does not have operational efficiency and focus on the regions where economies of scale work towards their favour.

Shareholder oriented management and activist investor on the board.

TCI Fund Management, led by Sir Christopher Hohn, accumulated a position of just over 9% in Cellnex by early 2023, making it the company’s single largest shareholder ahead of both the Benetton family’s Edizione and Singapore’s GIC. The stake was built deliberately across direct shares and derivatives, giving TCI substantial economic exposure before it became a visible force on the shareholder register.

The immediate catalyst for TCI’s public intervention was Cellnex’s botched CEO succession following the departure of founding chief executive Tobías Martínez. Hohn wrote directly to the board in March 2023, declaring that the search had been mishandled and demanding the removal of three directors, including chairman Bertrand Kan. Within weeks, both Kan and director Peter Shore had resigned.

TCI’s representative Jonathan Amouyal was appointed as a proprietary director in April 2023 and, critically, placed on the Capital Allocation Committee. Amouyal spent over a decade at TCI specifically covering digital infrastructure and tower assets, meaning he arrived with deep knowledge of the precise levers that drive per-share value in this industry.

The impact on capital allocation has been direct and measurable. Under TCI’s influence, Cellnex formalised a €1 billion shareholder return programme comprising €500 million in dividends and €500 million in buybacks through end-2026, followed by a commitment to a minimum €500 million annual dividend growing at 7.5% per year from 2026 onwards. The buyback is being executed at roughly 14x EBITDAaL, against a private market clearing price of 20–24x, making each share retired mechanically accretive to intrinsic value per share. Simultaneously, the divestiture programme across Ireland, Austria, Sweden, Denmark, and now Switzerland which TCI’s capital allocation oversight helped accelerate. TCI recycled proceeds from subscale, low-return positions into debt repayment and buybacks, compressing leverage and expanding FCF simultaneously.

Compensation structure for Marco Patuno (CEO of Cellnex)

The most direct link is the explicit inclusion of cash shareholder remuneration as a standalone metric within the annual bonus. The 20% individual objective weighting tied specifically to dividends and buybacks means that Patuano benefits personally when capital is returned to shareholders. This compensation structure is absolutely unique and the first that I have seen in a company as most executive remuneration frameworks treat capital return as an output of financial performance rather than a performance metric in its own right.

The second mechanism is the LTIP’s dual total shareholder return structure. By measuring both absolute TSR and relative TSR against a defined peer group simultaneously, the plan ensures that Patuano’s long-term equity award only fully pays out if Cellnex shareholders have actually made money in absolute terms and have outperformed the alternatives they could have held instead. The compensation structure is as stated in their CEO remuneration investors package: LTIP carries a target opportunity of 183% of fixed remuneration, with a maximum of 275% of that target. The maximum opportunity would only be paid if the maximum achievement scenario was attained in the financial and sustainability metrics, and if Cellnex’s annualised and compounded absolute TSR was at least 20%, with Cellnex ranked first versus peers.

Patuno’s compensation structure is dependent on the following(from cellnex investors presentation):

For the annual bonus, each of the five metrics revenue growth, EBITDAaL, recurring leveraged free cash flow, adjusted net debt/EBITDA, and cash shareholder remuneration carries an equal 20% weighting, with threshold performance defined as follows: revenue growth must reach 95% of the budgeted target; EBITDAaL must reach 95% of target; RLFCF must reach 95% of target; adjusted net debt/EBITDA must be no worse than 103.13% of the target ratio (i.e. leverage can be marginally higher than planned but not materially so); and cash shareholder remuneration must reach 80% of the committed target. In each case, hitting threshold unlocks a payment level of 75% of target for that metric, while hitting maximum defined as 107.5% of budget for the financial metrics and 108% for shareholder cash remuneration unlocks 150% of target. Intermediate outcomes are calculated by linear interpolation.

In euro terms, that translates to the following payout schedule across scenarios:

At below-threshold performance, no LTIP is paid whatsoever. At threshold, the payout is 50% of target incentive (approximately €1.19 million). At target, the full 183% of fixed remuneration pays out approximately (€2.38 million). At maximum, the payout is 275% of that target incentive (approximately €6.54 million), deliverable entirely in Cellnex shares.

The third mechanism is the mandatory shareholding requirement, now set at three times fixed remuneration following the 2025 policy revision. At a fixed salary of €1.3 million, this requires Patuano to hold approximately €3.9 million of Cellnex stock on an ongoing basis. Combined with the LTIP being granted entirely in shares, his personal net worth is substantively exposed to the same price movements as any other shareholder. He cannot hedge through option asymmetry or extract value through a rising market while being insulated from the downside.

With current RLFCF yield sitting at close to 11% and normalised FCF yield (ex BTS capex) of 8.6%, we can be sure that management will be returning that FCF to its shareholders instead of doing dumb acquisitions considering that management incentives are aligned well with its shareholders.

To boost the RLFCF of the company, cellnex started celland. Its purpose is to convert the ground leases sitting beneath Cellnex’s towers from recurring annual costs into one-time capital investments, progressively shifting the company from tenant to owner of the land its towers sit on. Ground lease payments to landowners represent 15–25% of tower revenue which is a structurally large and growing cost line. These leases are typically denominated with annual escalation clauses, meaning that in an inflationary environment, the cost of sitting on that land compounds upward year after year with no corresponding benefit to the tower operator. Cellnex currently owns the land beneath fewer than 15% of its towers which is already the highest ownership proportion of any European towerco, but dramatically below the 40–70% ownership rates typical of US tower companies like American Tower and Crown Castle. Cellnex targets to buy back land from farmers/landowners at approximately equivalent to ten years of rental payments, a significant outlay at face value. But Cellnex’s ground leases are predominantly structured as 25–30-year commitments with escalation clauses, meaning that over the full life of the lease, the cumulative rental payments would far exceed the purchase price. By converting the leases into an appreciating asset and also having the ability to raise prices at CPI +escalators will enable the company to have significant operating leverage in the long run as the costs that cellnex is in charge of will not increase as much the revenue.

4) Continuous improvement in tenancy ratios as Colocation rates increase

Over the past 3 years, the tenancy ratio of cellnex has increased from 1.39x in 2023 to the current 1.6 in 2025. As the BTS orders are completed through 2030 (with the bulk of it completed by 2028), cellnex will add an additional 10K sites which will bring their total tower portfolio to 122K from 113K currently. However these new BTS towers will have a dilutive effect on the tenancy ratios as the new BTS towers only have a tenancy ratio of 1. Despite the dilutive effect of the new towers that are coming online, management is still guiding a tenancy ratio of over 1.7 by 2030.

To put into perspective on whether this is feasible, we can compare it to the American tower counterparts who also have a dominant market share in their respective markets. Tower companies in America such as AMT and crown castle are most likely the most representative when comparing to cellnex given that it is what Europe will likely achieve in the future as it. The tenancy ratios are 2.6X and 2.5X respectively for each company. Considering that the markets that cellnex operates in such as Italy, France and Spain have similar market structure for the telco companies (3-4 major operators) it is not unfeasible for cellnex to obtain such ratios in the distant future.

In my DCF model, I will assume that cellnex will hit a 2.5X in tenancy ratios by 2050 and maintain at those tenancy ratios for the years to come.

Common Worries By Investors

High Debt Levels

Some investors might point to the high debt levels and say that it is a cause of worry, whilst I tend to avoid high debt companies, I make an exception for cellnex due to the following reasons.

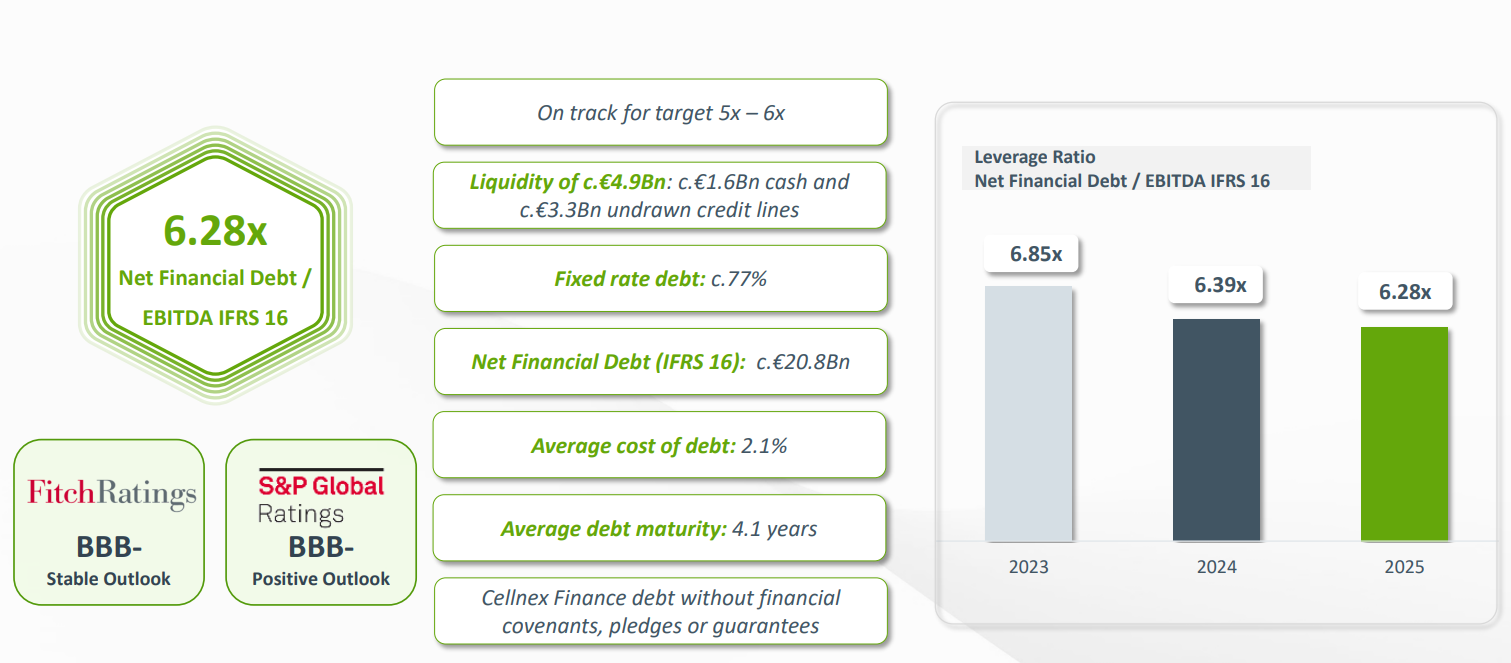

Cellnex has a stable recurring revenue that is not cyclical in nature. The visibility of the revenue and underlying profits and FCF are clear due to the contractual nature of the company. In situations like this where the company is able to invest in upgrades and build more towers to generate a leveraged ROI of 15-20% and borrow at an interest cost of 2-3%, it is a no brainer to saddle the company in debt. Furthermore, to alleviate investors concerns of the high debt levels, the management has set a target Debt/EBITDA of 5-6X to ensure that the company remains investment grade that will enable the company to refinance their debt at a more affordable rate.

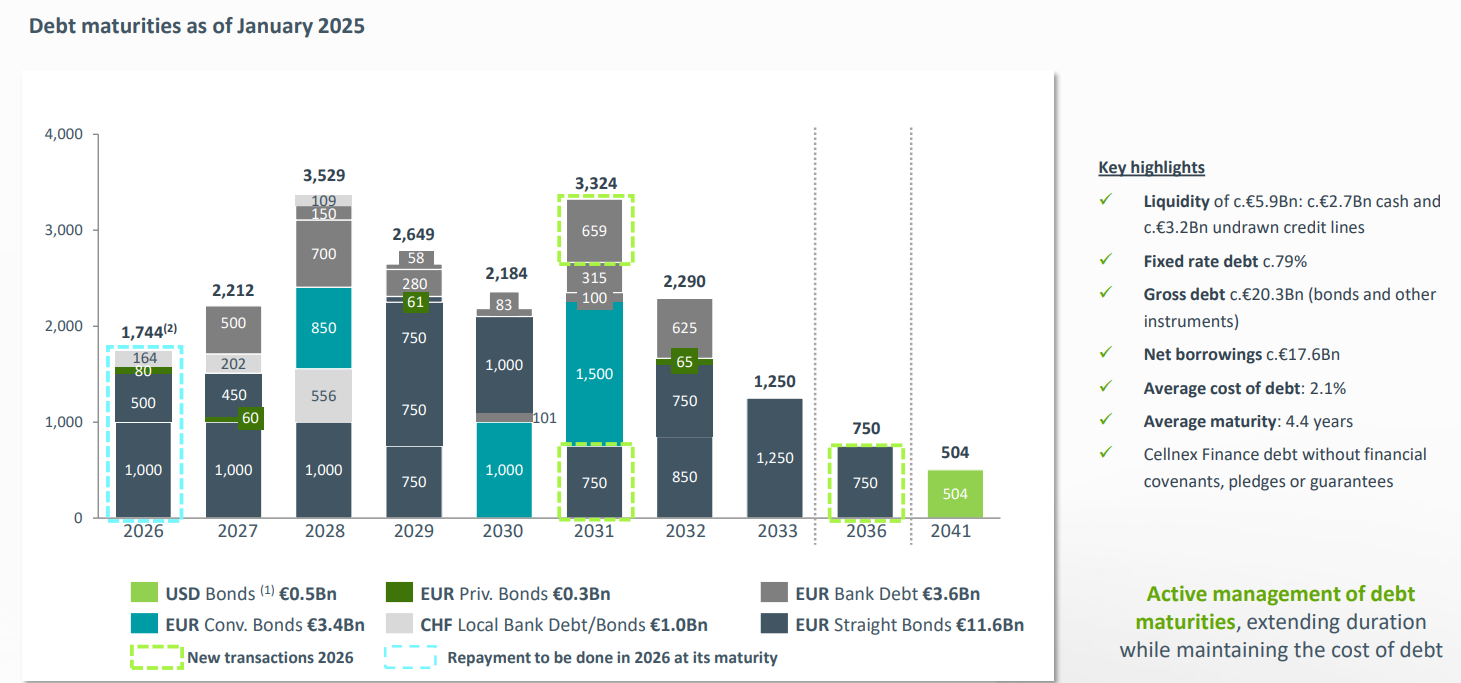

The company also has strong liquidity and does not face refinance risk till 2027. Furthermore, based on management’s guided RLFCF in 2027, the company is expected to maintain 2.1B in RLFCF despite the divestiture of some of its towers. If push comes to shove, cellnex will be able to cease all growth capex to cover the upcoming debt obligations required. The 2.1% average cost of the debt is also an asset to the company considering that current refinance rates for the company are at 3.2%. Considering that the company also has 2.7B in cash and is able to pay down 2.1B in debt a year if they cease all growth and expansionary capex, the likelihood of the company going bust is near 0 and the current high debt levels is maintained due to the management’s decisions instead of them being unable to pay the debt off (as seen from management using the 1B capital from the disposal of their assets to buyback shares instead of paying down debt).

Another key risk that investors are worried about is the recent trend where MNO (mobile network operator) consolidation in Europe is also another factor that is worrying the investors. The wave of European MNO consolidation MasOrange in Spain, VodafoneThree in the UK, and Fastweb/Vodafone Italia in Italy is the single most discussed risk factor among investors in Cellnex and European towercos more broadly. The concern is intuitive: if two mobile operators merge, they previously occupied two sets of tower slots, and post-merger they theoretically need only one. The worry is structural churn, the permanent loss of a co-location tenant who is no longer a separate entity. But the reality is considerably more nuanced, and the investor debate spans several distinct dimensions. The first and most immediate concern is network rationalisation churn. Towercos face real challenges from the increasing consolidation of European mobile markets, such as MasOrange in Spain and VodafoneThree in the UK. When two operators merge, the combined entity will almost always find sites where both networks have overlapping coverage, and on those sites it will eventually decommission one of the two tenancies.

However, in reality what we do see is that there is limited churn due to the special clause in cellnex’s contracts. When a mobile operator merges with a competitor, the merged entity inherits two sets of tower contracts one with each legacy operator’s towerco arrangements. Left unconstrained, the merged operator could selectively retain the towers it deems strategically valuable from each portfolio, cherry-picking the best sites from Cellnex while exiting the less commercially attractive ones. This selective churn would be the worst possible outcome for a towerco as it would lose its highest-density urban sites while retaining only marginal rural towers with weak economics. The merged operator would effectively extract maximum value from the towerco’s portfolio while minimising its own contracted obligations.

The all-or-nothing clause under cellnex’s contracts eliminates this optionality entirely. Under its terms, a merged operator cannot selectively exit individual towers from a Cellnex contract; it must either maintain the entirety of its contracted tower portfolio or exit the entire portfolio in one single transaction. The clause converts what would otherwise be a gradual, unpredictable erosion of tenancy into a binary, negotiated event. Cellnex either keeps all of an operator’s towers or loses all of them, and losing all of them triggers a contractually defined termination payment that compensates Cellnex for the full present value of the remaining contracted cash flows on every surrendered site.

The practical consequence is that a merged MNO faces an enormous financial barrier to any churn. Walking away from a Cellnex contract under an all-or-nothing structure requires paying termination fees across potentially thousands of sites simultaneously which is a capital outlay that in most realistic scenarios exceeds the cost saving the merged operator would achieve by rationalising duplicate coverage. The clause therefore functions not just as compensation protection but as a strong economic deterrent to churn in the first place.

The MasOrange situation in Spain is the clearest live illustration of how this operates in practice. When Orange Spain and MásMóvil (both are mobile network operators) merged to create MasOrange, they became Cellnex’s single largest Spanish customer, sitting across contracts originally negotiated separately with each legacy operator. Rather than facing a wave of unilateral site withdrawals, Cellnex negotiated a comprehensive settlement: the 1,027 site withdrawals that appeared in the FY2025 results were not unilateral exits but negotiated reductions agreed as part of a broader contract restructuring that simultaneously extended the MasOrange relationship through 2048 with an all-or-nothing clause on the remaining portfolio and unlocked thousands of additional contracted PoPs (points of presence) through expanded RAN sharing arrangements with Digi. The churn was compensated, the duration was extended, and the remaining portfolio was ring-fenced with even stronger contractual protection than existed before the merger.

As other MNOs start to merge together, it is unlikely that this dynamic will be impacted and it is highly likely that cellnex will still be able to maintain the low churn rate that it is currently enjoying of 1.2%.

Valuation

Cellnex’s 2026 guidance puts RLFCF between €1.9 and €2.0 billion, giving a midpoint of €1.95 billion as the base year.

Our valuation is anchored to Recurring Levered Free Cash Flow (RLFCF), which we treat as the most appropriate metric for a business of Cellnex’s profile. Unlike net income, which is heavily distorted by depreciation on a vast asset base, or EBITDAaL, which abstracts away the cost of capital, RLFCF captures the actual cash the business generates for equity holders after servicing its debt, paying its taxes, and funding the maintenance and efficiency capital necessary to sustain the portfolio. It is the number that funds dividends, buybacks, and deleveraging, and therefore the number that should anchor any honest assessment of intrinsic value.

We use management’s 2026 guidance midpoint of €1.95 billion as the base year RLFCF. From this base, we apply 11% annual RLFCF growth through to 2028. This rate reflects two concurrent tailwinds that are already visible in the operating numbers: first, the continued clearing of the Build-to-Suit (BTS) backlog, which systematically converts committed capital expenditure into revenue-generating sites; and second, the operational efficiency programme that management has been executing since 2024, including the voluntary redundancy plan in Spain and the industrialisation of site management processes. These are already flowing through results, with EBITDAaL margins expanding from 60.6% in 2024 to 62.2% in 2025.

From 2029 to 2030, we step the RLFCF growth rate down to 7%, reflecting the natural deceleration as the BTS pipeline matures, offset by the compounding benefit of rising colocation ratios. As the tenancy ratio progresses beyond its current 1.6x, each incremental co-location tenant adds revenue at approximately a 95% margin, creating a structural tailwind for cash flow conversion that persists even as top-line growth moderates. Applying these assumptions, we arrive at a 2030 RLFCF of approximately €2.75 billion.

On revenues, we assume 5% annual growth through 2028, consistent with the contractual escalator mechanisms embedded in Cellnex’s MSAs and the organic volume growth from BTS completions and new co-locations both of which are already in evidence as seen from FY2025 revenues growing 5.8% organically. Beyond 2028, we moderate the revenue growth assumption to 3%, reflecting a more mature portfolio where incremental site construction decelerates but the colocation-driven mix shift continues to improve cash flow conversion at the margin level.

To arrive at a terminal equity value, we apply an 8% RLFCF yield on the 2030 RLFCF figure, implying a terminal value of approximately €34.4 billion. An 8% yield is a deliberately conservative exit assumption. The 10-year Bund, the long-run risk-free rate anchor for European infrastructure, sits materially below this level, and comparable tower assets have traded in private markets at implied yields of 4%. Using an 8% yield therefore builds in a substantial margin of safety against rate risk and mean-reversion uncertainty, making it a more defensible anchor for intrinsic value than a private-market-style multiple.

To this terminal equity value, we add the present value of the cumulative capital returns that accrue to shareholders over the holding period. Under Cellnex’s committed capital allocation policy, shareholders receive a €500 million dividend in 2026, growing at a minimum of 7.5% per year thereafter through 2030. In addition to dividends, we model buybacks of €300 million in 2026, €500 million in 2027, and €1 billion per year from 2028 onwards to 2030.

The mechanical significance of the buyback programme cannot be overstated. Aggregating dividends and buybacks over the five-year period yields cumulative capital returns of approximately €6.7 billion to shareholders, which represents over 30% of the current market cap. Aggregating the present value of the €34.4 billion terminal equity value and these cumulative capital returns and dividing it by today’s current share count, we cleanly capture the value per share.

Discounting the terminal equity value back at an appropriate rate and adding the present value of capital returns, we arrive at an intrinsic value estimate in the range of €42 to €47 per share on a fully diluted basis, against a current market price in the mid to high €20s. This implies an upside of approximately 45–60% to intrinsic value before accounting for any significant multiple re-rating toward private market levels. The key sensitivity in the model is the exit yield assumption; if the multiple rerates to a 6% RLFCF yield, which is still above where comparable private market transactions have cleared, the intrinsic value rises above €55 per share. The range of outcomes under realistic assumptions is therefore consistently above the current price, with downside scenarios requiring both a permanent derating of infrastructure assets and an extended period of rate pressure to threaten the thesis materially.

Potential near term catalyst

Cellnex is currently in talks to sell its 72% stake in its Swiss tower unit to Manulife Investment Management, the global asset management arm of Manulife Financial Corporation. The Swiss unit manages approximately 6,000 sites across the country, and Manulife has been working with financial advisors on a possible transaction.

JPMorgan analysts have estimated the entire Swiss unit’s value at approximately €2 billion, with the remaining 28% held by Swiss Life Asset Managers. Cellnex’s 72% stake would therefore imply a transaction value in the region of €1.44 billion for its portion alone. Cellnex entered the Swiss market in 2017 when it acquired Sunrise subsidiary Swiss Towers for €430 million meaning the implied exit price represents more than a 3x return on the original entry cost across the full unit, and a meaningful premium to book value.

This follows a previous attempt to sell the Swiss operations last year to EQT, which CEO Marco Patuano confirmed were halted due to bids not meeting the company’s expectations which clearly shows that Cellnex has pricing discipline and is not a forced seller, which strengthens its negotiating position. Third, the proceeds, if a deal is reached, would be recycled into further debt reduction and shareholder returns, consistent with TCI’s capital allocation framework and directly accretive to RLFCF per share as leverage compresses.

Should the sale of Cellnex’s Swiss towers be successful, we expect there to be meaningful share buybacks similar to the buybacks that the company had done after the sale of Austria towers as well as its data center business in France. Any news of the sale of the swiss division will likely cause the company to rerate upwards.

Impressive writeup!