Portfolio Returns & Reflections

Investment framework & returns so far

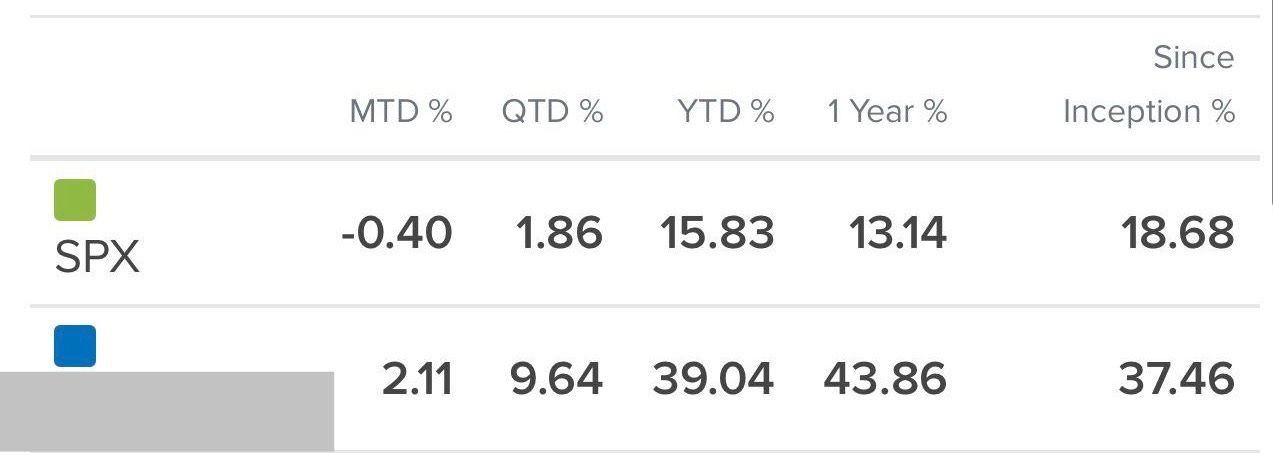

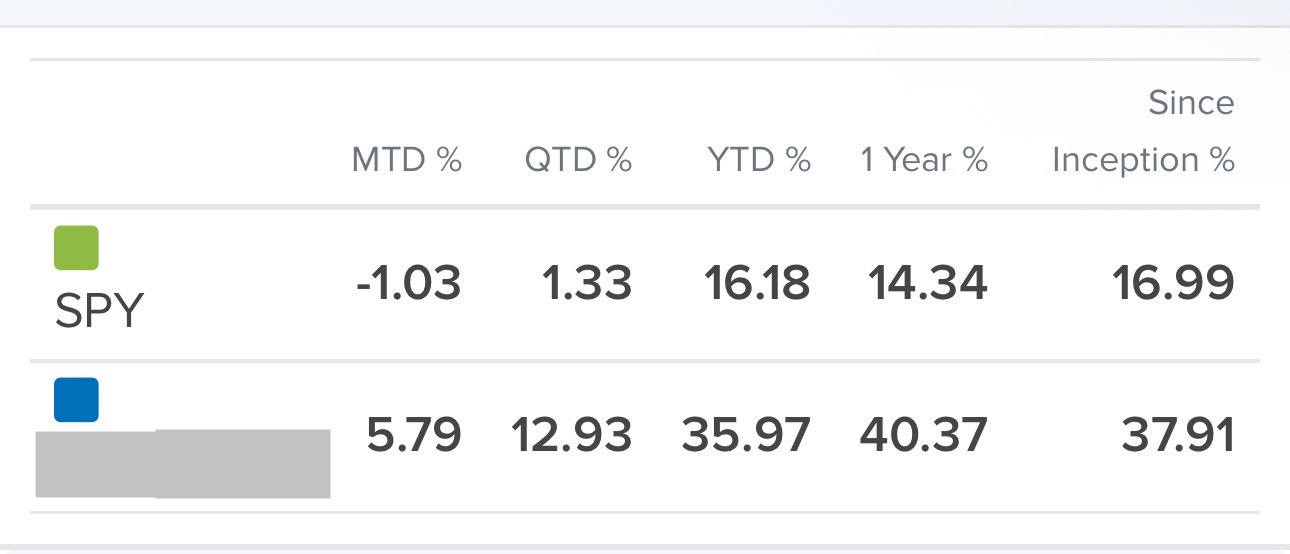

This will be a brief writeup on our investment returns and how we have generated these returns for the portfolio. Both of our portfolios are 6 figures which makes these returns meaningful.

Since our investment philosophy is quite similar, I have taken the liberty to reflect why we are able to outperform the market significantly over the past few years.

Do note that our portfolios started at different periods. I started this account about 2 years ago and Guan Rui started his about 1.7 years back. Hence we have slightly different annualised returns since inception. Both of us have been investing for 4+ years and we have other brokerage accounts before starting our IBKR account. We still remain invested in our other portfolios.

Whilst we share similar philosophies, we do not have the same positions within our portfolios and we also do not have the same portfolio allocation to each stock. It is pure coincidence that our returns are extremely similar but it is just testament of the replicability of our returns via our investment philosophy and framework.

We are lucky to have encountered the virtues of value investing and the tenets that Buffet and other investors have laid out.

Most investors would deem that their ideas are “old” and not replicable in today’s day and age but you have to remember that the lessons that they have written down are just investment frameworks and lenses that you have to further refine yourselves. Of course the age of net-nets are not relevant, neither is their investment in blue chip stamps nor Cities Service Preferred relevant in todays day and age but certain investment philosophies are timeless and should be utilised more often.

1) Always look for downside protection

Too many in today’s day and age are looking for quick returns. They turn towards momentum stocks hype stocks that have 0 fundamentals or a huge story where profits could be attained way down the line. Too few are looking at the downside and they always seek to make a quick buck and trade in an out of stocks. Guanrui and I have a different approach to investing and we (or at least I) focus on downside protection. In my portfolio this year, I had 3 large winners that utilised this investment lens.

HCC (+98% since initial entry @ 43)

Google (+107% avg price: 156)

ASML (+60% avg price: 650)

In each of these scenarios there was strong downside protection.

1) Warrior Met Coal had close to 0 debt, was trading with 20% of the market cap in cash and had mines that were valued at 7-8B via independent 3rd party appraisers compared to the market cap of 2B.

2) Google cloud itself would be valued at 160/share in 2030 using a DCF valuation. Even if search was disrupted and its value goes to 0, Youtube GCP and the cash position that google had already represented 70% of the market cap that google was priced at that point in time. Google was a no brainer and both guanrui and I loaded up on it and has contributed significantly to our returns.

3) ASML’s installed base management by itself was worth around USD 170 a share, with large buybacks from management coupled with a strong secular tailwind of protectionism, strong demand for chips fuelled by the AI boom and the impenetrable moat that ASML has, the downside of the company was limited.

Downside protection begins with a very simple but easily forgotten truth: the game is won by avoiding the mistakes that permanently destroy capital. Everything else ie returns, compounding, growth only happens after you’ve ensured survival. That starts with choosing businesses that can endure adversity: companies with durable competitive advantages, consistent demand for their products, and management teams that allocate capital with discipline rather than excitement. But downside protection is not only about the business, it’s also about how you approach valuation. The price you pay determines the protection you have. When you buy at a level that already reflects conservative assumptions, a wide margin of safety is baked into the investment. Even if your estimates are slightly wrong, the downside remains capped while the potential upside remains intact. This is why understanding the full range of outcomes and not just the base case is critical. You want situations where the worst-case scenario is survivable and the probabilities are skewed in your favour. Whilst I am delighted that the upside has worked out in my positions, I also do know that even if they did not work out, I will not lose much (Heads, I win. Tails, I don’t lose much).

Downside protection is a mindset of humility. It acknowledges that the future is uncertain, forecasts are imperfect, and you will inevitably be wrong at times. Too many investors buy into companies purely looking at the reward without considering the risks that they are taking. It is only a matter of time that such an investment style leads to large losses and we have no interest nor intention in making such losses.

2) Concentrate on your best ideas

Too often you hear investors boast, “I doubled my money on that investment!”—as if the return alone proves brilliance. But the moment you ask how much they actually committed, it usually turns out to be a just 1–2%, barely enough to matter. It’s empty victory chest-thumping, not real investing. When capital is spread thinly across numerous holdings, the marginal contribution of each position diminishes, effectively diluting the impact of rigorous research and informed judgment.

When an investor identifies opportunities in businesses and industries they understand well, and those opportunities are available at prices that offer a substantial margin of safety, failing to allocate capital meaningfully is stupid. However, the reverse is equally true: concentrating heavily in a position without a deep grasp of the company’s fundamentals and the industry’s competitive dynamics is equally idiotic. Concentration is justified only when both analytical understanding and valuation discipline are firmly in place. For my portfolio, I concentrate in my best ideas. Currently the top 5 holdings in my portfolio account for 74.2% of my entire portfolio and I hold only 12 positions in my portfolio. ASML GOOGLE HCC are all in my top 5 holdings and I have recently added 2 new positions in my top 5 holdings which will be disclosed in due date.

3) Quality over value

Quality matters more than value because a truly exceptional business compounds for you, while a merely “cheap” business demands that you constantly monitor, hedge, and eventually exit.

Remember value can only be ascertained via a DCF model which requires you to predict the future cash flows that a company can generate. However such cash flows are fleeting and “value” as calculated using a DCF is flawed and can only be used as an indicator. In a poor quality business where cash flows are unstable, forecasting the cash flows is a fools errand and completely useless.

A high-quality firm with durable competitive advantages, pricing power, and strong reinvestment opportunities increases its intrinsic value every year. That means time becomes your ally: the longer you hold it, the more the business works on your behalf. In contrast, a low-quality or structurally weak company might look statistically cheap, but without the ability to reinvest profitably or defend its position, its intrinsic value stagnates or erodes. Any gain relies on a re-rating or some temporary mispricing closing—events you cannot control.

Quality also reduces downside risk. Businesses with predictable earnings, conservative financing, and strong competitive positions are far more resilient in recessions. Their cash flows don’t vanish in tough environments, so their intrinsic value is far less volatile. Cheap companies often appear “undervalued” only because the market is correctly discounting real risks—poor economics, weak management, cyclical exposure, or structural decline.

And, crucially, quality aligns with the most powerful force in investing: long-term compounding. A company earning high returns on capital and able to reinvest at similar rates transforms patient ownership into exponential wealth creation. Buying quality at a fair or even slightly premium price can outperform buying mediocre businesses at bargain valuations, because one continues to compound while the other forces you to repeatedly find the next “cheap” opportunity. In the long run, owning a growing compounding machine is far superior to renting a series of statistically cheap assets. In this sense, quality isn’t just preferable—it is the very foundation of durable long-term returns.

The lollapalooza effect comes when you buy high quality companies at cheap prices. The best returns come from companies where the markets in general do not recognise the presence of a moat. Warrior met coal is a case in point. The company has an indestructible moat that is cannot be replicated by any other company and is in an industry with a secular tailwind. Hidden moats are the best as you are able to benefit from the profits that the business generate without paying a premium as the markets do not price such businesses higher as they don’t recognise the moat that the business possesses. Even with a high price appreciation, it is highly likely that the returns will still remain decent over the next couple years as blue creek goes into full production.

4) Thou shalt not use excel -mohnish pabrai

Warren Buffet does not use excel. Thats not to say that we should not use DCFs as we are not like buffet who has memorised the compounding tables in his brain and is a math whiz.

My interpretation of Prabai’s quote as such:

If you need to constantly adjust or stretch the assumptions in your DCF just to make the numbers look attractive, then the investment simply isn’t undervalued enough to deserve meaningful capital. A truly compelling opportunity doesn’t require spreadsheet gymnastics. In the case of Warrior Met Coal, the company held cash equal to roughly 20% of its market cap, owned mines worth several billion, and was on track to generate around $400 million in free cash flow once Blue Creek comes online—yet the entire business traded at only about $2 billion. You don’t need Excel to recognise that warrior is undervalued. That being said, excel modelling is crucial and I use it for all my investments.

Would highly recommend beginners to read this book:

The Warren Buffett Stock Portfolio: Warren Buffett’s Stock Picks—Why and When He Is Investing in Them (2011)

In this book Mary buffet used warren’s basic investment framework to forecast prices of core positions in buffet’s portfolio and many of them 10 years down the line were trading +_10% of what was forecasted. This book is quite beginner friendly and the content covered is understandable.

I hope this brief writeup has been useful to you and helps you reevaluate your investment framework. It offers just a small glimpse into what Guan Rui and I consider when investing. There’s much more to it than what I could cover in 30 minutes, but hopefully it’s helpful. Of course there are other strategies that you can use as well. Catalyst investments/Deep Value turnaround plays etc can make you money but it is not our preferred style of investing. Guanrui will be doing a separate write up to supplement what is written here so do keep a lookout for it.

We haven’t posted the qualitative aspects that we look out for in a business yet so keep a lookout for it.

Thanks for explaining your investment strategy. I agree that downside protection and buying great companies at undervalued prices are crucial to investing success! Hopefully Mr. Market continues to give more such opportunities